.png)

Stablecoins have become one of the most important innovations in crypto. While Bitcoin and Ethereum dominate headlines with their volatility, it’s stablecoins that power most of the actual transactions, handling over two-thirds of all crypto volume. Their promise is simple but powerful: digital money that stays steady.

These assets are pegged to real-world values, usually the US dollar, and now form the backbone of many crypto and fintech systems. In the past year alone, stablecoins on public blockchains processed more than $30 trillion in settlements, reflecting how far they’ve evolved from niche trading tools into global financial infrastructure.

In this guide, you’ll learn what stablecoins are, why they matter, how they work, and which are the leading players across each category.

What Is a Stablecoin?

A stablecoin is a type of cryptocurrency designed to maintain a fixed value by being tied, or "pegged", to an external asset, such as the US dollar, gold, or even another cryptocurrency. The most common peg is 1:1 to the US dollar, meaning one stablecoin equals one dollar.

Stablecoins solve one of crypto’s biggest challenges: volatility. While Bitcoin can rise or fall 10% in a day, stablecoins aim to stay level. That makes them useful for payments, remittances, DeFi, and trading, anywhere reliability matters.

At its core, the stablecoin definition is simple: it is a class of cryptocurrency designed to maintain a stable value. Most commonly, this value is pegged 1:1 to a traditional fiat currency, such as the US Dollar. Unlike Bitcoin, which is often called the "digital gold," a stablecoin aims to be the "digital dollar" (or euro, yen, etc.). This makes them an essential bridge between the traditional financial world and the decentralized crypto space, serving as an on-chain medium of exchange and a reliable store of value.

The answer to "how do stablecoins work" lies in their stabilization mechanism, which generally falls into two primary categories, reflecting the two types of stablecoins:

How Do Stablecoins Work?

Stablecoins achieve price stability in one of five key ways:

- Fiat-collateralized, pegged to traditional currency and backed by reserves.

- Crypto-collateralized, backed by other cryptocurrencies, with excess collateral.

- Commodity-collateralized, backed by physical goods like gold.

- Algorithmic, rely on supply-demand algorithms without real reserves.

- Treasury-collateralized, backed by short-term government securities, sometimes offering yield.

*Some also clasify it simply in two types of Stablecoins: Collateralized and Non-collateralized.

1. Fiat-Backed Stablecoins

Simple, centralized, and dominant

Fiat-backed stablecoins are pegged to national currencies, typically the USD, and are fully backed by cash reserves, commercial paper, or short-term treasuries. They are issued by centralized entities that manage reserves and ensure convertibility.

Top Fiat-Backed Stablecoins:

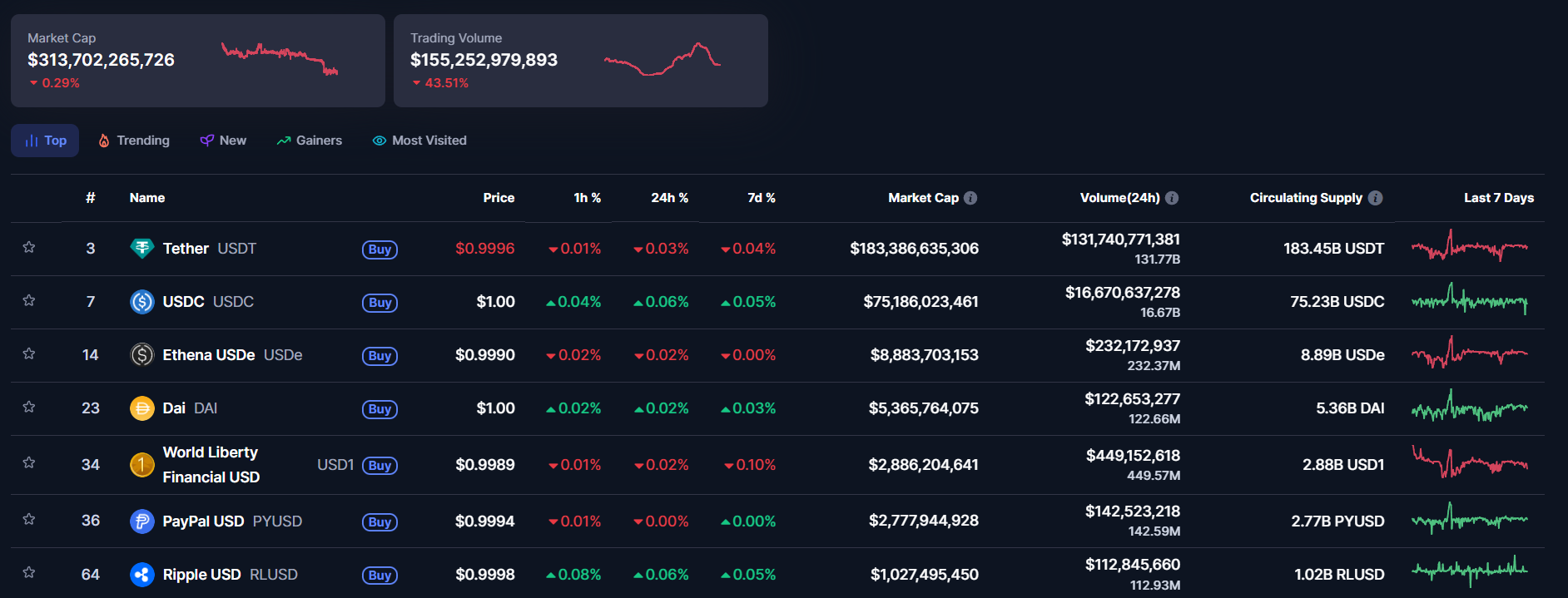

The most widely used stablecoin with over 183 billion USDT in Net Circulation. Operates on multiple blockchains and claims to be backed by a mix of cash, corporate bonds, loans, Bitcoin, Precious Metals and cash equivalents and other short term deposits. Widely used for trading and payments.

Issued by Circle and backed 1:1 by cash at reserve banks ($9.4B) and the Circle Reserve Fund ($65B) with a circulation of 75.9 billion USDC . Known for its transparency and partnerships with mainstream financial platforms.

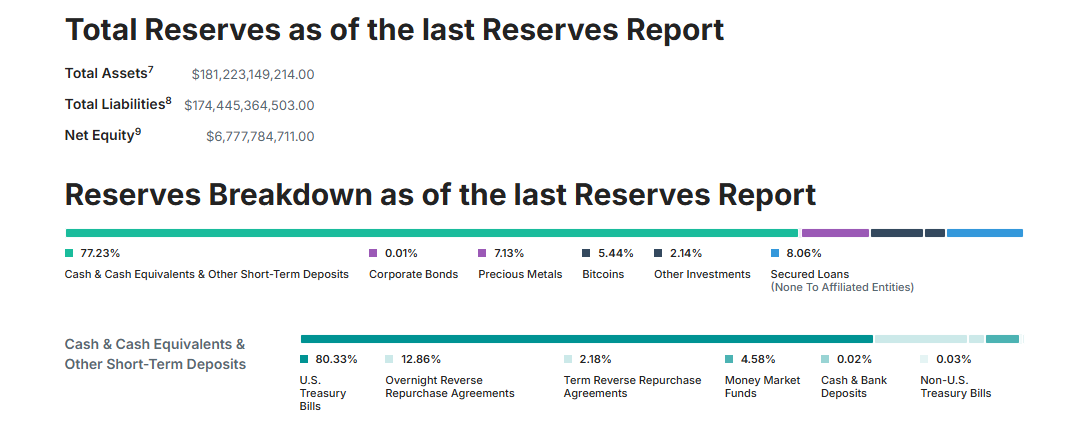

Co-founded by the Trump Family, with a circulating supply of $2,88 B and integration with 6 blockchains. USD1 Offers monthly attestations of its reserves and is used in some high-volume trading environments.

2. Crypto-Collateralized Stablecoins

Decentralized, over-collateralized, and trustless

Instead of fiat, these stablecoins use cryptocurrencies (like ETH or SNX) as backing. To account for the volatility of crypto, users must deposit more value than they mint. These systems often rely on smart contracts and are common in DeFi.

Top Crypto-Collateralized Stablecoins:

- DAI

Issued by the MakerDAO protocol and backed by Ethereum and other crypto assets. It is managed entirely on-chain through decentralized governance. - sUSD (Synthetix USD)

A synthetic dollar created within the Synthetix protocol, requiring a collateralization ratio of up to 500% in SNX tokens. - LUSD (Liquity USD)

Fully decentralized and over-collateralized with Ethereum. Known for its censorship resistance and low-interest loans.

3. Commodity-Backed Stablecoins

Asset-based, inflation-hedging tokens

These stablecoins are tied to tangible assets, most commonly gold. They're ideal for investors seeking inflation protection and physical asset exposure without the logistical challenges of custody.

Top Commodity-Backed Stablecoins:

- PAX Gold (PAXG)

Each token represents one troy ounce of gold stored in LBMA-approved vaults. Redeemable for physical gold. - Tether Gold (XAUT)

Offers gold exposure via the same company behind USDT. Each token is backed by one fine troy ounce of gold held in Switzerland. - DGX (Digix Gold Token)

A smaller player backed by physical gold bars, with full audit trails and transparent storage records.

4. Algorithmic Stablecoins

No collateral, pure code, high risk

These stablecoins use algorithms to expand or contract the token supply to maintain a price peg. Though theoretically elegant, many have failed in practice due to volatility and cascading liquidations.

Top Algorithmic Stablecoins:

- Ampleforth (AMPL)

Pegged to the 2019 USD CPI-adjusted dollar, it uses a “rebasing” mechanism to alter users’ balances daily based on price. - Legacy Frax Dollar (FRAX)

A partially algorithmic, partially collateralized stablecoin. It aims to balance decentralization with price stability. - Neutrino USD (USDN) (formerly active)

Pegged to the USD using a collateralization model based on WAVES tokens. Faced multiple depegging incidents.

⚠️ Note: Algorithmic stablecoins are inherently unstable and often collapse under stress, as seen with the infamous TerraUSD (UST) crash in 2022.

5. Treasury-Backed Stablecoins

Yield-bearing, regulation-friendly

These newer stablecoins are backed by short-term US Treasuries or money market funds, offering users both stability and returns. They're aimed at investors looking for low-risk yield in tokenized form.

Top Treasury-Backed Stablecoins:

- USDY (US Dollar Yield Token)

Backed by short-term Treasuries and bank deposits. Holders earn passive yield from underlying assets. - USYC

A compliant, yield-bearing stablecoin for institutional investors, backed by US government securities. - BUIDL (BlackRock)

Technically a tokenized money market fund rather than a stablecoin, but operates similarly. Offers daily liquidity and regulated oversight.

Top Stablecoins by Market Cap: A Shortlist for Secure Gaming

When selecting the best options for transactions and stablecoin staking on a platform like ours, market capitalization and reliability are paramount. These are the current leaders, forming the core stablecoin list:

| Stablecoin | MarketCap | Backing | Key Properties |

| USDT - Tether | $183.4 B | Fiat-Collateralized (Cash, T-Bills, Commercial Paper, etc.) | Dominant Market Share

High liquidity and broad exchange support |

| USDC - Circle | $75.2 B | Fiat-Collateralized (Cash & Short-term US Treasuries) | Transparency Focused

Known for high-quality, highly liquid reserves. |

| USDe - Ethena | $8.8 B | Synthetic Dollar (Delta-Neutral Staked ETH & Derivatives) | Yield-Bearing Innovation

Aims to be a censorship-resistant, capital-efficient, and scalable. |

| DAI - MakerDAO | $5.3 B | Crypto-Collateralized (On-Chain Assets) | Decentralized (DeFi Native) Governance-driven, relying entirely on smart contract code. |

| USD1 - WLFI | $2.8 B | Cash & U.S. Government Money Market Funds | Political & Institutional Focus

A major new entrant whose reserves are custodied by BitGo. |

| PYUSD - Paypal | $2.7 B | Fiat-Collateralized (Cash, T-Bills) | Consumer Integration Fully compliant, designed for mass adoption. |

| RLUSD - Ripple XRP | $1 B | Fiat-Collateralized (cash and cash equivalents) | The TradFi Bridge

Designed for institutional use, transaction settlement on the XRPL. |

| XAUT - Tether | $1.51 B | Commodity-Collateralized (Physical Gold) | Hard-Asset Backing

Represents ownership of one troy ounce of physical gold. |

What Are Stablecoins Used For?

Stablecoins have matured into key pillars of the global financial system. Their use now extends far beyond crypto exchanges into sectors like international finance, e-commerce, and real-world asset settlement.

- Cross-Border Payments & Remittances

Stablecoins offer a faster, cheaper alternative to traditional remittance systems, which average 6.6% in fees. Platforms like Bitso in Latin America now process millions in stablecoin-based transfers monthly. Transactions settle in minutes, 24/7, even on holidays.

- DeFi Lending, Staking & Liquidity

Stablecoins power the entire decentralized finance ecosystem. Users lend, borrow, and farm yield using stablecoins as collateral or base assets. Their consistent value makes them essential for liquidity pools and risk-managed strategies on platforms like Aave, Compound, and Curve.

- Trading & Market Hedging

With over 80% of exchange volume involving stablecoins, they are a critical hedge during market volatility. Traders move into USDT or USDC to preserve value without cashing out to fiat.

- E-commerce & Merchant Payments

Stablecoins are gaining traction as a payment method. Shopify now supports USDC via Coinbase, while Amazon and Walmart are exploring their own stablecoin launches. Compared to credit card fees of up to 3.5%, stablecoin payment networks offer ultra-low fees under 0.1%.

- Financial Access in Unbanked Regions

An estimated 25% of the global population lacks access to banking. With just a smartphone and internet connection, users in regions facing inflation or limited banking services can store value and participate in global finance via stablecoins.

- Tokenized Asset Settlement

Stablecoins are crucial for settling tokenized real-world assets (RWAs), such as tokenized treasuries. BlackRock’s BUIDL Token has over $1 billion in assets. The tokenized treasuries market now exceeds $4.2 billion, marking a shift toward institutional-grade blockchain finance.

How Stablecoins Could Drive U.S. Debt Demand

The rapid expansion of stablecoins is doing more than transforming payments and DeFi, it’s quietly reshaping global capital flows and amplifying demand for U.S. government debt.

Stablecoins and the Dollar's Digital Reach

Stablecoins function as digital extensions of the U.S. dollar, enabling access to dollar-denominated assets in regions where physical dollars are scarce or restricted. From Latin America to Sub-Saharan Africa, users increasingly turn to stablecoins like USDT, USDC, and USDY as financial lifelines.

This demand for stable digital dollars indirectly creates a new, global class of Treasury bill buyers, the stablecoin issuers themselves.

Treasury-Backed Stablecoins Need Safe Yield

Stablecoins backed by short-term U.S. Treasuries, like USDY, USYC, and BUIDL, require large reserves to maintain their pegs and generate yield. As user demand for these tokens grows, so does the need to purchase more Treasury securities. These reserves are no longer just parked in cash, they're actively placed in high-grade U.S. government debt.

As of 2025, stablecoin issuers hold over $120 billion in T-bills. Some projections suggest this number could rise to $660 billion, rivaling the U.S. Treasury holdings of major sovereign nations like China ($772 billion). Future reserve regulations could push this figure even higher, possibly creating up to $900 billion in new demand for short-duration government debt.

The Dollar as a Global Digital Asset

This phenomenon reinforces dollar dominance in a world where countries like China and Russia are pushing for “de-dollarization.” Ironically, digital finance may be accelerating the opposite. People bypass capital controls not by moving physical dollars, but by minting stablecoins, digital claims on dollar-backed reserves.

Implications for U.S. Fiscal Policy

The U.S. government, facing rising deficits and borrowing needs, could benefit from this stablecoin-fueled demand. If a significant portion of the world adopts stablecoins for commerce, savings, and finance, it effectively turns global users into indirect supporters of U.S. debt markets, helping absorb Treasury issuance and potentially reducing borrowing costs.

Are Stablecoins Safer Than Money in the Bank?

This is a powerful question that gets to the heart of the stablecoin value proposition. Many of the largest fiat-backed stablecoins are collateralized 1:1, meaning the issuer, such as Tether or Circle, claims to hold 100%+ of the asset value in cash or highly liquid equivalents like short-term US Treasury bills.

Contrast this with the traditional commercial banking system:

- Commercial Banks (Fractional Reserve Banking): Banks operate on a fractional reserve system, where they only hold a small percentage (historically 0-1%, though self-imposed requirements may be 10-15%) of customer deposits in reserve. The rest is loaned out. If all depositors demanded their money back, a "bank run", the bank simply does not have the cash on hand to meet those withdrawals.

- Stablecoin Issuers (Full Reserve Model): Issuers like Circle operate on a full-reserve or 100%+ model, which is fundamentally different. Their stated goal is to be able to redeem every USDC (or USDT) for $1 on demand, 24/7, irrespective of the time of day or bank holidays. In a purely collateralized sense, holding money in these tokens is theoretically safer than holding an uninsured deposit at a regional bank.

It is no secret that the banking lobby fears stablecoin adoption and the rise of stablecoin yield products. As crypto exchanges offer users ways to earn a modest return on their stablecoin holdings, there is a legitimate concern that this could drive withdrawals from low-interest or zero-interest bank accounts. Traditional banks are concerned they are not in a capacity to face in numbers the large-scale shift of deposits into fully backed, 24/7 accessible digital cash.

However, a crucial point of nuance must be addressed: stablecoin collateralization is not entirely separate from the banking system. Issuers still rely on major commercial and custodian banks to hold the cash deposit portion of their reserves. Thus, while your USDC or USDT may be safer than your regional bank's uninsured deposit because the stablecoin issuer promises 1:1 redemption from its regulated reserve, the stability of that reserve is still partially reliant on the underlying financial institutions.

Ultimately, the transparency offered by major issuers, combined with the promise of 24/7 accessibility, positions the top stablecoins as a compelling and secure alternative to holding fiat cash in the traditional system. The ongoing push for clear regulatory frameworks, such as the proposed Clarity for Payment Stablecoins Act in the US, aims to cement this trust and provide a definitive stablecoin bill for the future.

Stablecoins, Dollar Lifeline or Trojan Horse?

Stablecoins have unlocked digital dollar access for millions of users around the world, offering fast, low-cost payments, protection against local currency instability, and on-chain financial tools unavailable through traditional banks. They’ve become essential infrastructure for cross-border commerce, DeFi, and tokenized assets. For many, they represent a financial lifeline.

But their design comes with trade-offs.

Most of today’s dominant stablecoins, such as USDT and USDC, are issued by centralized companies and are mutable by design. Issuers can freeze or blacklist addresses, even when funds are stored in a hardware wallet, and may comply with regulatory demands instantly. Because these tokens are ultimately tied to the U.S. dollar, they also inherit its monetary inflation. While this makes them convenient mediums of exchange, it also means they are not ideal long-term stores of value. In many ways, they operate like private, programmable dollars, powerful, but permissioned. They resemble CBDCs in everything but official status.

On the other hand, decentralized stablecoins such as DAI or LUSD take a different approach. They are backed by on-chain crypto collateral rather than bank accounts, governed through decentralized protocols, and are significantly harder to freeze or censor. However, they come with their own trade-offs: slightly lower acceptance across exchanges, liquidity fragmentation, and reduced influence on U.S. Treasury markets. Their value proposition centers around user autonomy and censorship resistance over convenience and regulatory alignment.

Across all categories, one trend is clear: stablecoins deepen global reliance on digital dollars. Treasury-backed models now hold well over $100 billion in short-term U.S. debt, and growing. As adoption accelerates, this indirect demand could continue to support U.S. borrowing needs for years to come.

Yet stablecoins are not the end state of crypto finance. As awareness of fiat dilution grows, capital still seeks scarce assets like Bitcoin, gold, productive land, and other inflation-resistant stores of value. Stablecoins serve as a bridge, linking traditional money systems to decentralized markets, providing stability today, while enabling users to pursue greater financial sovereignty tomorrow.

Brought to you by Flush Crypto Casino & Sportsbook

At Flush Casino, you’ll find the best place to play top slot machine games, live casino classics, and much more, all available for real money. As a premier Bitcoin casino, we provide a smooth, secure way for players to enjoy their favorite games using cryptocurrency. Our extensive collection includes slots from world-renowned providers like Pragmatic Play, Play’n GO, NoLimit City, Hacksaw Gaming, Big Time Gaming, Yggdrasil Gaming and many more.

Alongside these, Flush offers exclusive in-house games, Flush Originals, designed to put you in control of the risk, reward, and ultimately the thrill of the game. From fast-paced multiplayer hits like Crash and Dice to strategic challenges like Mines, Dragon Tower, and Video Poker, these Originals bring unique experiences you won’t find anywhere else.

Flush also delivers a complete real money online casino experience, including live dealer games like Poker, Blackjack, Baccarat, Roulette, and exciting game shows. Whether you're using Bitcoin or another cryptocurrency, we make it easy to deposit, play, and cash out securely, making Flush the perfect destination for crypto casino enthusiasts.

And now, with the launch of Flush Sportsbook, you can Bet on everything from the UEFA Champions League and NBA to UFC, Formula 1, and eSports like Dota 2, CS2, League of Legends, Fifa and multiple e-fighting games, all with the same smooth crypto-powered experience. Packed with live stats, expert tips, and a powerful Bet Builder, Flush Sportsbook makes every wager more exciting.

If you're new at Flush, the welcome offer is straightforward: 150% match on the first deposit, ceiling of $1,500, 1× deposit wagering on the welcome itself. Weekly Races run automatically on slot spins.

Flush brings Bitcoin and traditional casino play together in one place. Browse the slot library, claim the welcome offer, and start with a deposit in BTC, ETH, USDT, or any of the other supported coins. Crypto deposits clear in minutes and withdrawals settle on the same network you came in on.

.png)

.png)

.png)

.png)

.svg)

.png)

.png)